Grants and Contracts

When administering Grants and Contracts, General Accounting works closely with the Office of Research and Sponsored Programs (ORSP), in addition to the faculty and staff who direct and manage UNC's research projects and other sponsored programs. General Accounting is responsible for:

- Setting up awards in the Banner system

- Assigning fund numbers

- Reviewing expenditures and monitoring compliance

- Preparing financial report and invoices

- Coordinating audit reviews and closing out funds

- Preparation of the Facilities and Administrative proposal and negotiation

- Preparation of the Fringe Benefit proposal and negotiation

Sponsored Programs (Grant) Accounting Guidelines and Procedures

- What accounting does

- In the beginning

- Provide fund and grant number to ORSP

- Upon receiving fund application form (FAF) and documentation from ORSP

- Setup new grant award in Banner

- Setup Indirect Costs

- Enter budget in Banner

- During your performance period

- Process journal entries to adjust expense, as allowable

- Review and approve all PCard transactions on your grants

- Review and approve all invoices paid on your grant

- Monitor and request cash from your federal sponsor

- Invoice non-federal sponsors

- Monitor your Indirect Cost (IDC) charges, will adjust via journal entry as allowable

- Prepare and file all financial reports related to your grant, this will be a collaboration with ORSP and PI, as applicable

- Answer all financial questions

- Near the end

- The PI and Accounting Specialist will analyze budgets and submit final expenses

- Upon request, General Accounting moves expenses in or out of grant, based on allowability

- Final IDC checks

- Draw final cash on federal awards

- Send out final invoices on non-federal awards

- Close out fund, on request by ORSP

- In the beginning

- Document flow

What should be sent to Grant Fund Accountant:

- Journal entries

- PCard statements (via Purchasing)

- ACH/Check requests (via Accounts Payable)

- ALL deposits to Restricted Funds

- 36 federal grant funds

- 35 federal grant funds

- 32 non-federal grant funds

- 32 and 33 Foundation funds

- Any questions about invoices, charges or financial information

What should be sent to ORSP:

- All budget change requests

- All In-Kind documents

- All labor redistribution

- Requests for no cost extensions (NCEs)

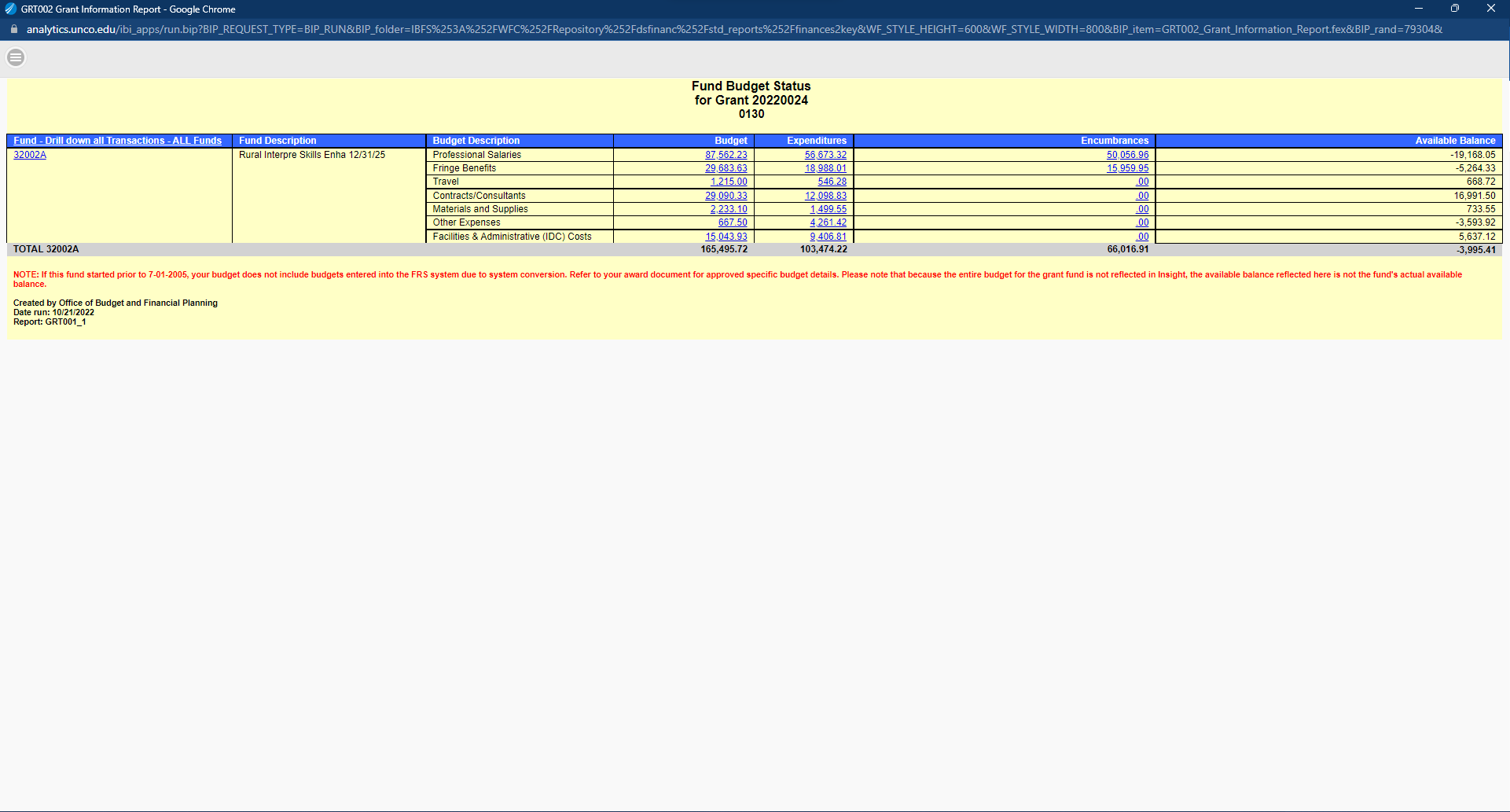

- Budget Monitoring

- This report can provide summary or detail level data.

- Looks at life of grant

- Rolls expenses into budget categories

- Indirect Costs (IDCs) will affect your available budget, these are calculated monthly.

- Payroll is encumbered for the calendar year, even if your grant ends before December 31st.

- Although there can be some flexibility between categories, the total amount to spend is not flexible.

- Will include expenses with incorrect ORGs

- Has the ability to pull all funds ties to a Grant number (multiple funds, match funds, etc.)

- When in doubt, please ask. We are here to help.

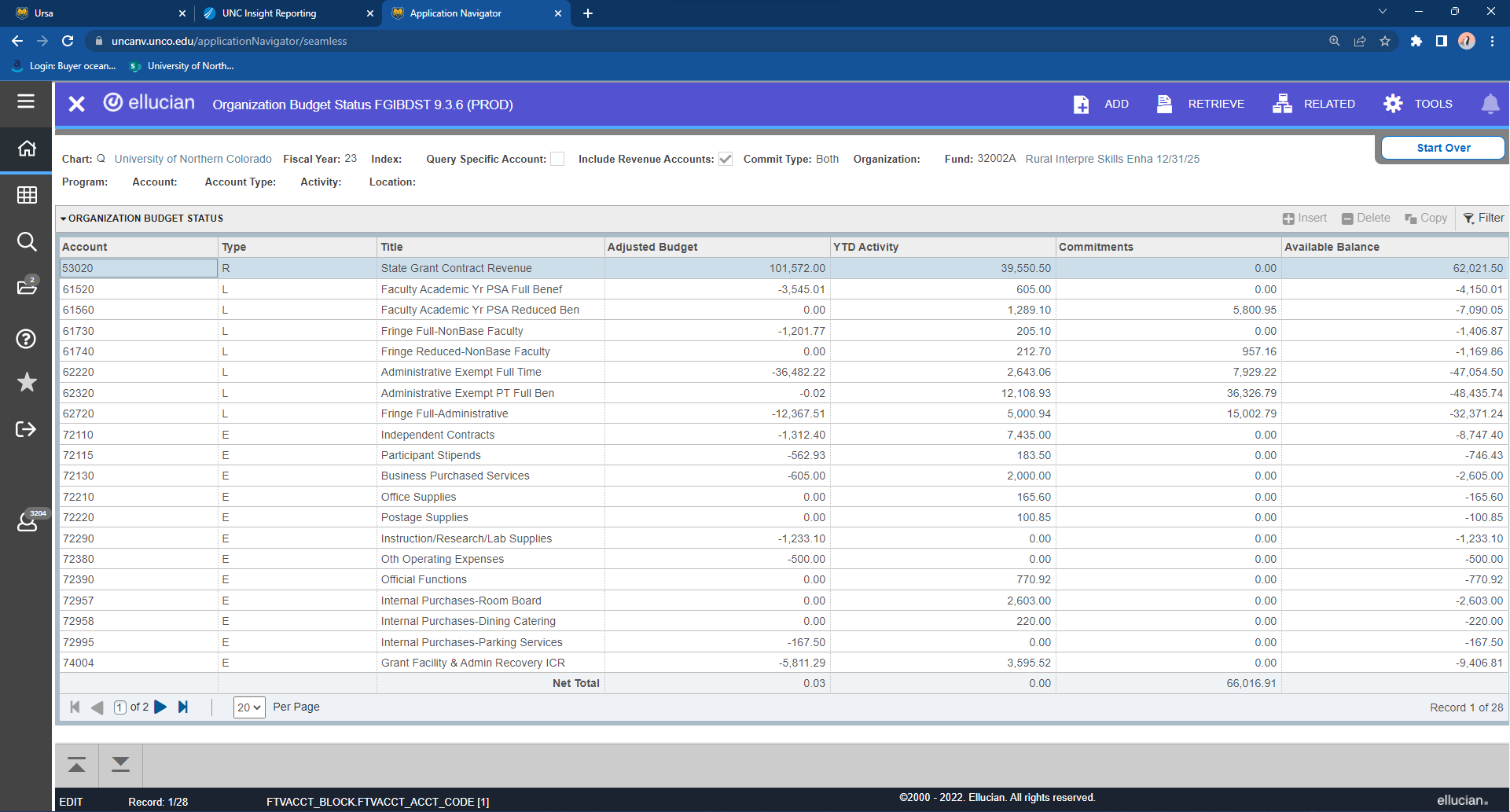

- Real time information

- Looks only at a fiscal year

- Budget does not line up with expense

- Revenue is NOT cash

- Payroll encumbered for entire calendar year

- Expenses with wrong Org will not show in Banner

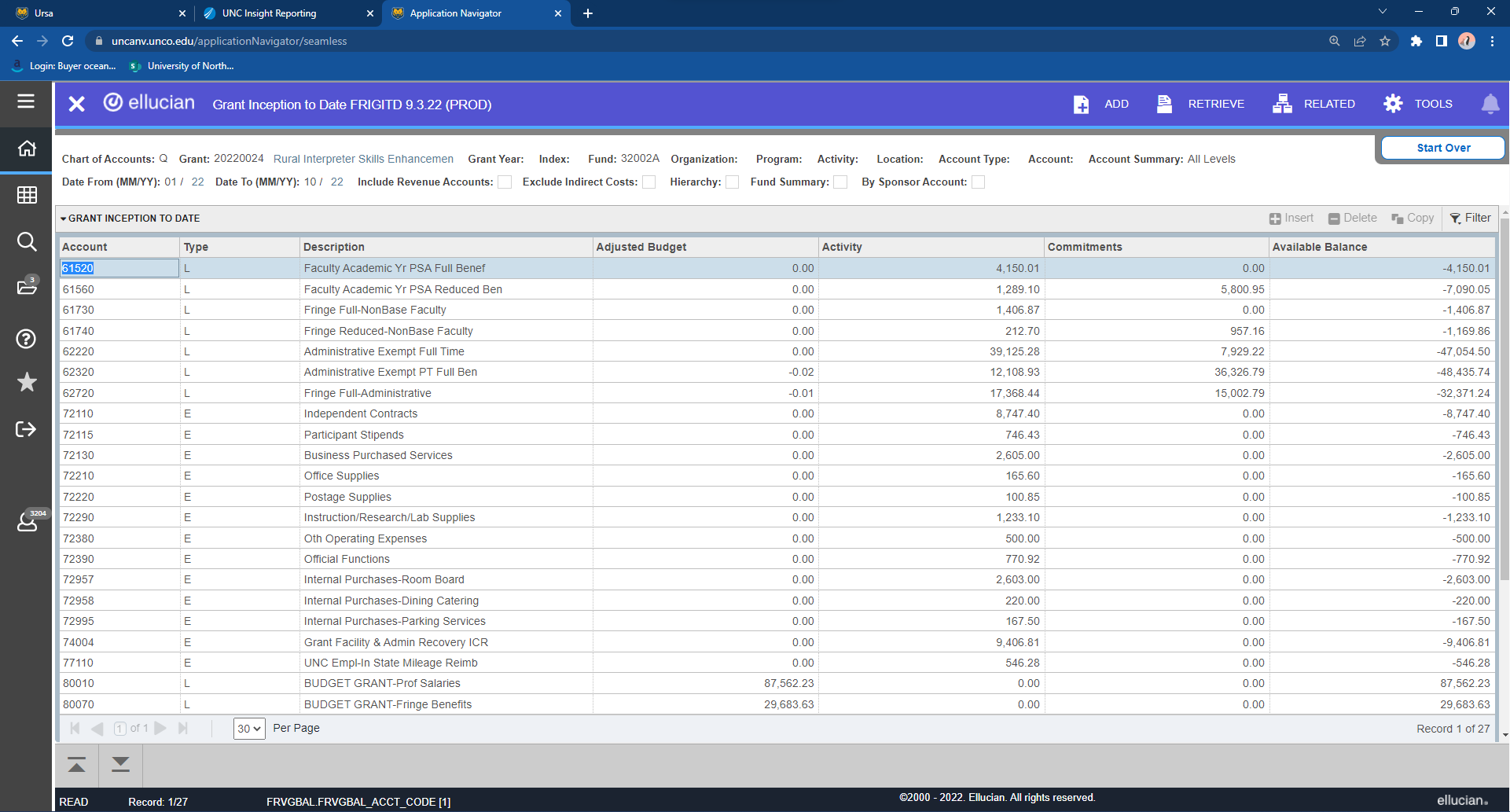

- Real time information

- Looks at life of grant

- Can pull all funds tied to Grant number (multiple funds, match funds, etc.)

- Expenses with wrong Org will not show in Banner

- Indirect Costs

Indirect costs represent the expenses of doing business that are not readily identified with a particular activity, but are necessary for general operation of the organization.

Indirect costs are those costs that are not classified as direct. Direct costs generally include:

- Salaries and wages

- Fringe benefits

- Consultant services

- Travel

- Materials, supplies, and equipment

The Indirect Cost Rate:

- Is a Federally negotiated rate - 38% for FY23

- Varies by grant (often less than our negotiated rate)

- IDC expense is calculated by Banner and posted to grant fund monthly, as a percentage of direct costs, IDC expenses post to account code 74004

- 30% of IDC revenue distributed to college as "Research Incentive"

- Progress and Financial Reports

Progress Reports:

- PI will work with ORSP on the budget narrative and schedules

- Financial (expense) data can only be provided by Grant Accounting

- PI writes narrative for work completed

- PI or ORSP submits, depending on your award

- Can be certified by the PI and/or ORSP

Financial Report:

- General Accounting will file invoices, Federal Financial Reports (FFR's), all other

financial reports including quarterly, semi-annually, annually and final

- Can be collaborative process with PI and ORSP

- Normally submitted by General Accounting

- In some specialty cases, we will ask the PI to review the transactions and category totals prior to sending the report

- During the reporting process, we reconcile cash, expense, match and in-kind to budget

- Financial reports will always be certified by General Accounting, typically by the University Controller or the Senior Accountant

- Foundation Accounting

Foundation Funds:

- Foundation funds are numbered 328xx - 329xx

- These funds do not run off of budget in Banner but are on a reimbursement basis with the Foundation

- Expenditures are pulled by General Accounting on a monthly basis

- Example: In November, October expenditures are pulled and invoiced to the Foundation for reimbursement

Things to remember:

- The proper Fund, Org, Account, and Program numbers are necessary for expenses to be processed

- Expenses posted to Foundation funds require an Activity Code (X1234). Without the Activity Code, the Foundation will not know where to post the expense

- The person(s) with signature authority over the Fund/Org combination at the University needs to be aware of the donor intent for this restricted money and how it can be used

Contacts

Accounting Office:

Jeff Martin - 970-351-1830

Director of ORSP

John Hamill III - 970-351-1932

Sponsored Projects Officer

Pamela Keener - 970-351-4388

Donations, Gifts and Grants UNC Foundation -

970-351-2034

Development and Alumni Relations - 970-351-2551

{kind=link}

{kind=link}

{kind=link}